PM Apna Ghar Program 2026

The PM Apna Ghar Program 2026, also known as the Wazir-e-Azam Apna Ghar Program with the tagline Ghar Ho Tu Apna, is a government-backed housing finance initiative designed to change that reality. It provides low-markup loans with flexible repayment options so that ordinary citizens from every part of Pakistan can finally purchase or construct their own home.

This program is not just a financial product. It is a national commitment to reducing homelessness and boosting the construction sector, which in turn creates jobs and stimulates economic activity. Whether you live in a major city or a rural district, this scheme opens a clear and affordable path to homeownership. Understanding how it works, who can apply, and what documents you need is the first step toward making use of this opportunity.

What Is the PM Apna Ghar Program 2026 and Who Launched It

The PM Apna Ghar Program 2026 is a federal housing initiative operating under the Markup Subsidy and Risk Sharing Scheme for Affordable Housing Finance. The government has partnered with all major commercial banks, Islamic banks, microfinance banks, and the House Building Finance Company Limited to make this scheme nationwide and accessible. The tagline Ghar Ho Tu Apna reflects the simple vision of this program, which is to put a roof over every deserving family’s head.

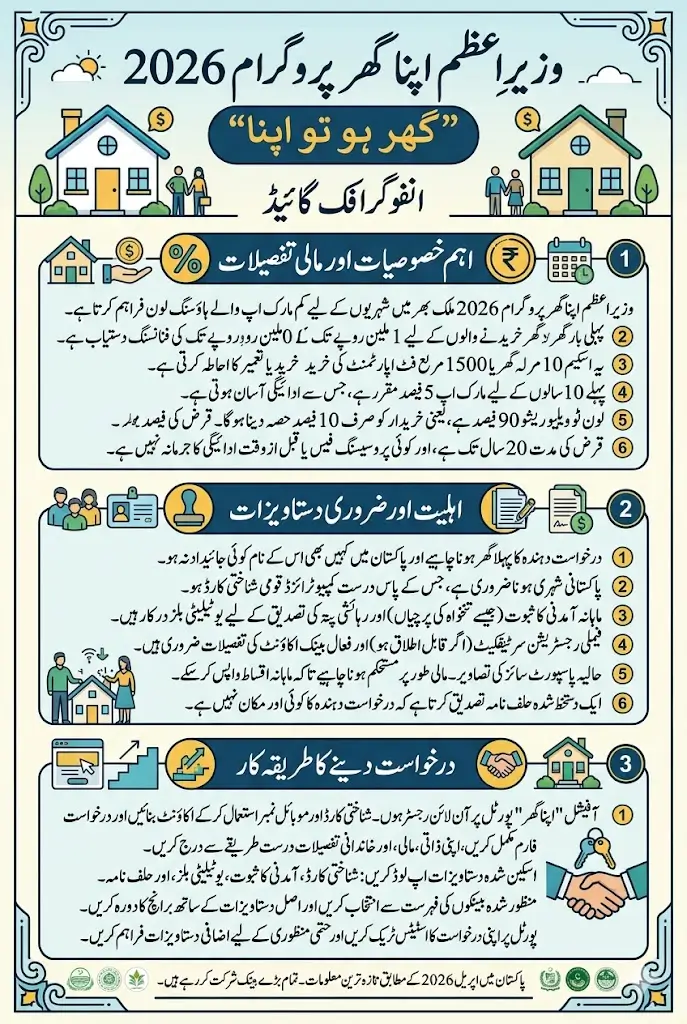

The scheme provides financing of up to Rs. 10 million for first-time homebuyers who wish to purchase or construct a housing unit of up to 10 Marla or a residential apartment of up to 1,500 square feet. The markup is fixed at 5 percent for the first ten years, and then shifts to market rate for the remaining period of the loan tenure. This makes the initial repayment phase far more manageable for low and middle-income borrowers who need stability in their monthly installments.

Who Is Eligible to Apply for the PM Apna Ghar Scheme

Eligibility under this program has been defined with care to ensure that benefits reach those who genuinely need them. The most fundamental requirement is that the applicant must be a first-time homebuyer with no existing housing unit registered in their name anywhere in Pakistan. This condition ensures the scheme serves those who are truly seeking to own a home for the first time rather than expanding existing property holdings.

Beyond property ownership status, applicants must hold a valid Computerized National Identity Card and must be Pakistani citizens. Financial stability is also evaluated, as the applicant must demonstrate a reasonable capacity to repay monthly installments over the loan tenure. Special consideration is given to women, widows, and differently-abled individuals, making the program more socially inclusive and aligned with the broader welfare goals of the government.

Key Features and Financial Details of the Housing Loan

Understanding the financial structure of this program helps applicants plan their application and repayment strategy more effectively. The loan is structured to keep the burden minimal in the early years while ensuring long-term recovery. With a loan-to-value ratio of 90 percent, the borrower only needs to contribute 10 percent of the property value upfront, which significantly reduces the initial financial pressure.

| Loan Feature | Detail |

|---|---|

| Maximum Financing | Rs. 10 million |

| Loan Tenure | Up to 20 years |

| Fixed Markup Rate | 5% for first 10 years |

| Remaining Years Markup | Market rate after 10 years |

| LTV Ratio | 90% bank financing / 10% borrower contribution |

| Property Size Limit | 10 Marla or 1,500 sq ft apartment |

| Processing Fee | None |

| Prepayment Penalty | None |

| Scope of Financing | Purchase or construction of housing units |

Applicants are advised to confirm exact markup rates and updated terms directly with their chosen participating bank at the time of application, as conditions may be subject to revision.

Documents Required Before You Begin the Application

Before submitting your application, it is critical to gather all the necessary documents in advance. Incomplete or inaccurate documentation is one of the most common reasons for delays or outright rejection.

Authorities use your submitted documents to verify your identity, financial standing, and property ownership status, so every detail must be accurate and up to date.

- Valid Computerized National Identity Card (CNIC) of the applicant

- Proof of monthly income such as salary slips or business income statement

- Recent utility bills for residential address verification

- Family Registration Certificate (if applicable)

- Active bank account details for fund processing and disbursement

- Recent passport-size photographs of the applicant

- Signed affidavit confirming the applicant does not own any property

Applicants should prepare scanned digital copies as well as physical originals of all these documents. Keeping everything organized ahead of time will save significant effort once you begin the formal registration and bank application process.

Step-by-Step Method to Apply for PM Apna Ghar Program 2026

The application process for the PM Apna Ghar Program involves both an online registration component and a direct engagement with a participating financial institution.

- Visit the official Apna Ghar Program online portal

- Create a new account using your CNIC number and registered mobile number

- Log in to the portal and open the application form

- Enter your personal and financial details carefully

- Fill in all required sections including:

- Full name

- Residential address

- Family information

- Employment status

- Monthly income

- Upload scanned copies of required documents such as:

- CNIC

- Proof of income

- Utility bills

- Property ownership affidavit

- Review all entered information to avoid mistakes

- Submit the application form

- Save your confirmation message or tracking ID

- Choose a participating financial institution from the approved list

- Visit the selected bank branch

- Submit a physical application with original documents

- Track your application status through the online portal

- Provide additional documents if requested within the deadline

- Receive final approval notification

- Proceed with loan agreement and property documentation

Following each step systematically and maintaining prompt communication with your chosen bank throughout the process is essential. Delays most often occur when applicants are slow to respond to verification requests or fail to submit complete documentation from the start.

Participating Banks and Financial Institutions for This Scheme

One of the strongest aspects of the PM Apna Ghar Program 2026 is the broad network of participating financial institutions. The government has ensured that applicants across different regions and financial preferences can access this scheme through a bank of their choice.

| Bank Name | Bank Name |

|---|---|

| ALBARAKA BANK (PAKISTAN) LTD. | ALLIED BANK LTD. |

| ASKARI BANK LTD. | BANK ALFALAH LTD. |

| BANK AL-HABIB LTD. | BANKISLAMI PAKISTAN LTD. |

| DUBAI ISLAMIC BANK PAKISTAN LTD. | FAYSAL BANK LTD. |

| FIRST WOMEN BANK LTD. | HABIB BANK LTD. |

| HABIB METROPOLITAN BANK LTD. | JS BANK LTD. |

| MCB BANK LTD. | MCB ISLAMIC BANK LTD. |

| MEEZAN BANK LTD. | NATIONAL BANK OF PAKISTAN |

| SAMBA BANK LTD. | SINDH BANK LIMITED |

| SONERI BANK LTD. | STANDARD CHARTERED BANK (PAKISTAN) LTD. |

| THE BANK OF KHYBER | THE BANK OF PUNJAB |

| UNITED BANK LTD. | HOUSE BUILDING FINANCE COMPANY LIMITED |

| ASA Pakistan Microfinance Bank | HBL Microfinance Bank |

| Khushhali Microfinance Bank | Mobilink Microfinance Bank |

| LOLC MFB | U Microfinance Bank |

The House Building Finance Company Limited also participates, bringing decades of specialized housing finance experience to the scheme.

How This Program Supports Economic Growth Beyond Housing

The PM Apna Ghar Program goes far beyond simply providing homes to deserving families. When thousands of housing units are constructed under this scheme, the demand for cement, steel, bricks, paint, electrical fittings, and labor rises significantly. This stimulates production across multiple industries and creates employment opportunities in both skilled and unskilled categories, which is particularly important for a country with a large working-age population.

Additionally, the development of new housing colonies and residential units drives investment in surrounding infrastructure such as roads, schools, and healthcare facilities. Local businesses near newly developed areas also grow as more families move in and consumer demand increases. The long-term economic ripple effect of such a large-scale housing initiative ensures that the benefits are not limited to homeowners alone but extend across the entire national economy.

Final Words

The PM Apna Ghar Program 2026 is a genuine and structured opportunity for Pakistani families to step out of rental dependence and into the stability of homeownership. With a transparent application system, affordable markup rates, a long repayment tenure, and no processing fees, the government has removed many of the traditional barriers that kept housing finance out of reach for ordinary citizens.

If you meet the eligibility criteria, the best step you can take is to gather your documents, visit the official portal, and connect with a participating bank as soon as possible. Opportunities like this require timely action, and being well-prepared from the beginning makes the entire journey far smoother.

Frequently Asked Questions

What is the maximum loan amount available under the PM Apna Ghar Program 2026?

The maximum financing available under this program is Rs. 10 million, which covers the purchase or construction of a housing unit up to 10 Marla or a residential apartment up to 1,500 square feet.

What markup rate will I pay on this housing loan?

A fixed markup rate of 5 percent applies for the first 10 years of the loan, after which the rate shifts to the prevailing market rate for the remainder of the loan tenure.

Q3. Is this scheme available to people who already own property?

No, this scheme is exclusively for first-time homebuyers who do not currently own any housing unit anywhere in Pakistan, which is verified through NADRA records and a signed affidavit.

Q4. Are there any processing fees or penalties involved in this program?

There are no processing fees and no prepayment penalties under the PM Apna Ghar Program, making it a genuinely cost-effective and borrower-friendly housing finance option.

Q5. Which banks can I approach to apply for this loan?

All major commercial banks, Islamic banks, and microfinance banks are participating, including Habib Bank, Meezan Bank, MCB, Bank Alfalah, United Bank, National Bank of Pakistan, and the House Building Finance Company Limited, among many others.